All Categories

Featured

Table of Contents

Life insurance coverage gives 5 economic benefits for you and your household. The primary advantage of including life insurance policy to your financial plan is that if you die, your beneficiaries receive a lump amount, tax-free payment from the policy. They can use this cash to pay your last costs and to replace your income.

Some plans pay if you establish a chronic/terminal health problem and some give financial savings you can utilize to sustain your retired life. In this short article, learn more about the different benefits of life insurance coverage and why it might be a great idea to purchase it. Life insurance offers benefits while you're still active and when you pass away.

How do I get Living Benefits?

Life insurance policy payouts normally are income-tax complimentary. Some permanent life insurance coverage plans construct cash money worth, which is money you can take out while still active.

If you have a policy (or policies) of that size, individuals who depend on your earnings will certainly still have money to cover their ongoing living costs. Recipients can make use of plan benefits to cover critical day-to-day expenses like lease or mortgage settlements, energy expenses, and groceries. Ordinary annual expenditures for households in 2022 were $72,967, according to the Bureau of Labor Data.

Life insurance policy payouts aren't considered revenue for tax obligation objectives, and your recipients don't have to report the money when they submit their tax obligation returns. A recipient may receive gained passion if they pick an installment payout choice. Any kind of rate of interest gotten is taxed and need to be reported as such. Depending on your state's legislations, life insurance policy benefits might be used to offset some or every one of owed inheritance tax.

Growth is not impacted by market conditions, enabling the funds to gather at a stable price over time. Furthermore, the cash money value of whole life insurance expands tax-deferred. This suggests there are no earnings tax obligations accrued on the money value (or its growth) till it is taken out. As the cash money worth develops up over time, you can use it to cover costs, such as getting a vehicle or making a down repayment on a home.

What is the difference between Cash Value Plans and other options?

If you decide to obtain versus your cash money value, the financing is exempt to earnings tax as long as the policy is not surrendered. The insurance provider, nevertheless, will charge passion on the lending quantity till you pay it back. Insurance provider have differing rates of interest on these lendings.

For instance, 8 out of 10 Millennials overestimated the price of life insurance policy in a 2022 research. In reality, the typical price is closer to $200 a year. If you believe buying life insurance policy may be a wise economic step for you and your family, think about seeking advice from a monetary advisor to embrace it into your financial strategy.

What is Premium Plans?

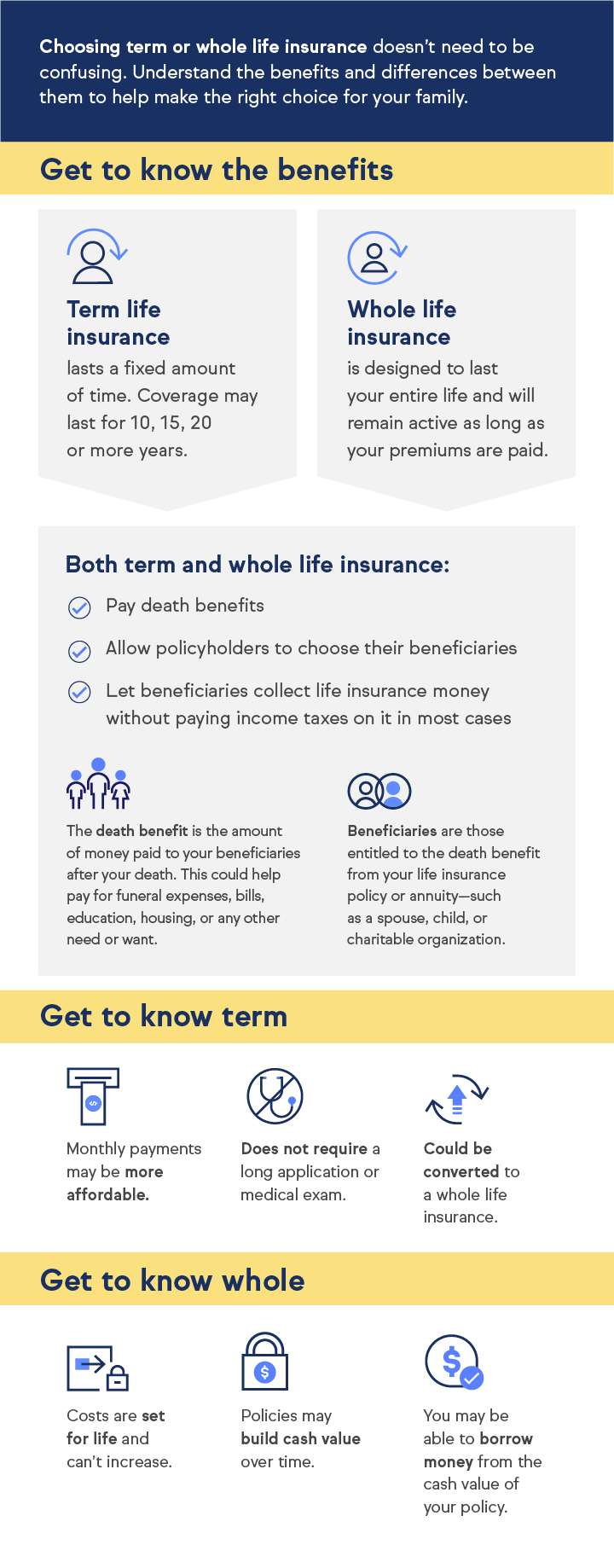

The five major types of life insurance are term life, whole life, global life, variable life, and last cost coverage, additionally referred to as burial insurance coverage. Each type has various attributes and advantages. Term is a lot more cost effective however has an expiration day. Whole life starts costing much more, however can last your whole life if you keep paying the premiums.

Life insurance coverage can additionally cover your mortgage and offer money for your household to keep paying their costs. If you have family depending on your income, you likely need life insurance to sustain them after you pass away.

Lesser amounts are readily available in increments of $10,000. Under this plan, the elected coverage takes impact 2 years after enrollment as long as costs are paid throughout the two-year duration.

Protection can be extended for approximately 2 years if the Servicemember is entirely impaired at separation. SGLI protection is automatic for most active service Servicemembers, Ready Reserve and National Guard participants scheduled to execute a minimum of 12 durations of inactive training per year, members of the Commissioned Corps of the National Oceanic and Atmospheric Management and the general public Wellness Solution, cadets and midshipmen of the U.S.

Who provides the best Death Benefits?

VMLI is readily available to Professionals who obtained a Specially Adjusted Real Estate Grant (SAH), have title to the home, and have a home mortgage on the home. shut to new enrollment after December 31, 2022. We began approving applications for VALife on January 1, 2023. SGLI insurance coverage is automatic. All Servicemembers with full-time protection ought to use the SGLI Online Registration System (SOES) to mark recipients, or minimize, decline or restore SGLI insurance coverage.

Participants with part-time protection or do not have accessibility to SOES should use SGLV 8286 to make changes to SGLI (Beneficiaries). Total and documents type SGLV 8714 or make an application for VGLI online. All Servicemembers should make use of SOES to decrease, lower, or restore FSGLI protection. To gain access to SOES, most likely to www.milconnect.dmdc.osd.mil/milconnect/. Members that do not have accessibility to SOES should use SGLV 8286A to to make adjustments to FSGLI insurance coverage.

What is the best Retirement Security option?

Policy advantages are minimized by any type of outstanding car loan or financing interest and/or withdrawals. Dividends, if any type of, are impacted by policy fundings and finance passion. Withdrawals over the price basis might lead to taxed ordinary earnings. If the policy gaps, or is surrendered, any exceptional lendings considered gain in the plan might go through ordinary income taxes.

If the policy owner is under 59, any taxed withdrawal might also be subject to a 10% federal tax penalty. Bikers may sustain an added expense or costs. Motorcyclists might not be readily available in all states. All entire life insurance policy policy warranties are subject to the prompt repayment of all needed premiums and the claims paying capacity of the providing insurer.

The cash money abandonment value, loan value and death proceeds payable will certainly be decreased by any lien exceptional as a result of the repayment of an accelerated benefit under this biker. The accelerated advantages in the first year show reduction of a single $250 administrative charge, indexed at a rising cost of living rate of 3% each year to the price of velocity.

A Waiver of Premium cyclist forgoes the obligation for the insurance holder to pay additional costs ought to he or she come to be entirely handicapped continually for at the very least six months. This motorcyclist will certainly incur an added cost. See plan contract for additional information and requirements.

How much does Level Term Life Insurance cost?

Learn extra about when to obtain life insurance policy. A 10-year term life insurance plan from eFinancial prices $2025 monthly for a healthy adult who's 2040 years of ages. * Term life insurance policy is more affordable than permanent life insurance policy, and women clients normally obtain a lower rate than male clients of the same age and health standing.

{kind=link}

Latest Posts

Instant Online Life Insurance Quotes

Final Expense Life Insurance Rates

Final Expense Insurance Agent